Oil Price Forecasts Amidst Conflict

Oil Prices: A History Written by Geopolitics

Oil isn’t just a commodity; it’s the lifeblood of modern civilization. But unlike corn or coffee, its price isn’t merely determined by crop yields or consumer taste. More than any other resource, oil prices are intrinsically linked to political stability, international conflict, and global security.

The relationship is simple yet profound. Oil production and transportation are concentrated in specific geographic regions, many of which are prone to political volatility. When conflict erupts, production is often shut in. Because of this vital supply routes are threatened, leading to immediate and dramatic price shocks.

The Past: A Chronology of Conflict

To understand this connection, we only need to look at historical data. For nearly half a century, every major spike in oil prices can be traced directly to a significant geopolitical event.

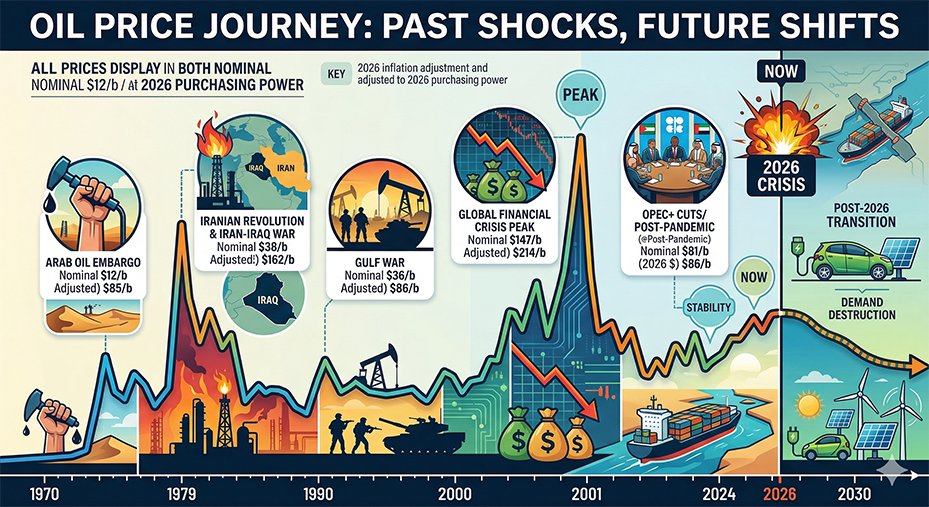

- 1973 Oil Embargo: Following the Arab-Israeli War, OAPEC (the Organization of Arab Petroleum Exporting Countries) implemented an oil embargo. This was the first major political weaponization of oil. Prices quadrupled from roughly $3 to nearly $12 per barrel. This created a global economic chaos and massive gas lines in Western nations.

- 1979 Iranian Revolution & 1980 Iran-Iraq War: The fall of the Shah of Iran and the subsequent invasion by Iraq disrupted a massive chunk of global production. Brent crude prices soared from around $14/b in 1978 to a peak of nearly $40/b in 1980.

- 1990 Gulf War: Iraq’s invasion of Kuwait and the resulting conflict immediately threatened Middle Eastern supply. While the disruption was shorter than previous crises, oil prices still spiked from $17/b to over $36/b in just a few months.

- 2003-2008 Iraq War and Beyond: A combination of sustained political instability in Iraq, growing global demand, and localized disruptions (like unrest in Nigeria) drove prices on a multi-year bull run. This period culminated in an all-time high of nearly $147/b in July 2008, a shock that many economists argue significantly contributed to the Global Financial Crisis later that year.

These events firmly established a market “fear factor” (or risk premium), where the mere possibility of conflict, especially in the Middle East, is sufficient to send prices higher.

The Great Divide: Oil Markets Before and After 2026

For a decade after the 2008 crash, oil markets experienced a phase of relative geopolitical calm, influenced by the emergence of the U.S. shale oil industry, which diversified global supply and added significant cushion. But this period of stability came to an abrupt end in 2026.

Before 2026: The Cushion

The first part of the 21st century (excluding the 2008 peak) was marked by a gradual normalization. The expansion of shale production meant that OPEC’s decisions to cut production had less dramatic effects. Prices hovered in a range, dropping severely during the COVID-19 pandemic in 2020 but stabilizing around $70-$80/b by 2024-2025. This era felt like the end of extreme geopolitical oil volatility.

But it was a false security. This stability relied on a delicate balance: that major disruptions wouldn’t occur simultaneously.

After 2026: The Crisis

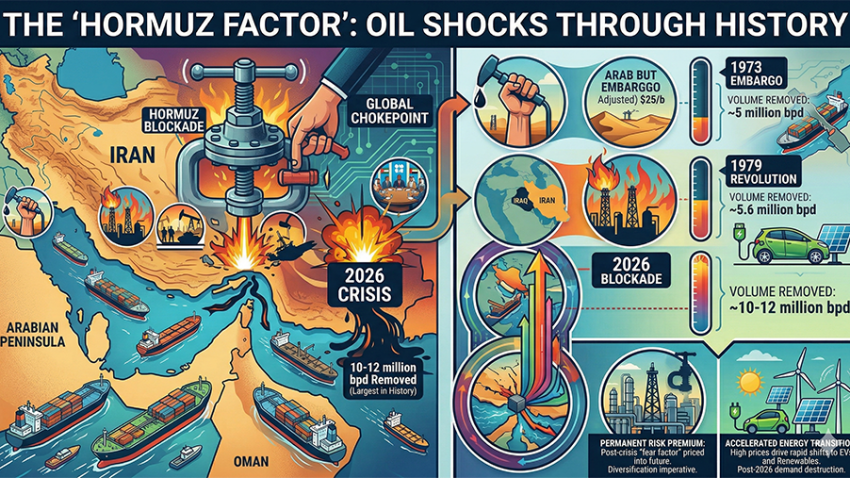

Everything changed in early 2026 with the outbreak of significant conflict in the Middle East. This wasn’t a localized skirmish; it was a systemic crisis that struck the very heart of global oil logistics.

The key turning point was the closure of the Strait of Hormuz on March 4, 2026. This vital 21-mile-wide waterway, through which nearly 20 million barrels of oil flow daily (approximately 20% of global consumption), was blockaded.

This single political action resulted in the largest and most sudden oil supply disruption in global history. The impact on prices was instant and violent. Brent crude, which had been stable at $69/b, immediately shot up, breaching $100/b and peaking at over $120/b as markets priced in a near-total loss of supply from major producers like Saudi Arabia, Iraq, and Kuwait. This event demonstrated, more clearly than ever, how a localized political event can instantly fracture the entire global energy system.

The Future: Navigating a New Energy Landscape

The 2026 crisis has reshaped the landscape of energy for decades to come. The future of oil prices now follows two distinct, parallel tracks: the path toward normalization of supply and the accelerated push for alternative energy.

The Price of Resilience

Looking at the immediate “post-crisis” period, analysts project a gradual cooling of prices, but a full return to pre-2026 levels is unlikely. This “new normal” includes a permanent risk premium.

Even if the Strait of Hormuz reopens and flows normalize (potentially by late 2026 or early 2027), the market memory of such a severe blockade will remain. Investment in new production from Western nations will increase as they prioritize “energy security” over cost, a strategic shift driven directly by this political shock. This diversification is costly, meaning that even when stability returns, oil prices are likely to settle at a structurally higher baseline (forecasted near $76/b in 2027) than the historical averages of the previous decade.

Accelerated Energy Transition: The Political Catalyst

Perhaps the most profound impact of the 2026 oil price crisis will be its effect on the energy transition. Political leaders worldwide, facing the immediate consequences of dependency on a single volatile fuel source, have radically accelerated their plans to diversify.

Before 2026, the adoption of electric vehicles (EVs) and renewable energy was driven primarily by environmental concerns. After 2026, the primary driver is national and energy security. The financial pain of $120/b oil has forced both consumers and governments to find alternatives.

- Accelerated EV Adoption: Consumer demand for EVs, once a niche market, has exploded. Markets that were previously seen as developing EV infrastructure are now fast-tracking these projects. Projections for EV market share have been pulled forward significantly. By 2027, EVs are forecast to make up 35% of all new car sales, rising rapidly to over 50% by 2030—a milestone previously not expected until much later.

- Grid Modernization and Renewables: Massive investments are being channeled into domestic renewable energy sources (wind, solar) and grid infrastructure to reduce reliance on imported oil for all sectors, not just transportation.

This forced evolution is creating a phenomenon known as “demand destruction” for oil. While supply shocks caused by politics push prices up in the short term, this accelerated transition puts structural, long-term downward pressure on oil demand—and consequently, on prices—as we approach 2030. The 2026 crisis, though politically driven, has inadvertently set the stage for an era where oil’s dominance as the global energy workhorse will rapidly diminish.

Historical Price Shocks: Nominal vs. Real (2026 Dollars)

When we adjust for inflation, we see that the 1970s and 2008 weren’t just expensive—they were economically tectonic.

| Event | Year | Nominal Price | Equiv. in 2026 Dollars |

| Arab Oil Embargo | 1973 | $12/b | $85/b |

| Iranian Revolution | 1979 | $38/b | $162/b |

| Gulf War | 1990 | $36/b | $86/b |

| Global Financial Peak | 2008 | $147/b | $214/b |

| Modern Stability Era | 2024 | $81/b | $86/b |

| Current Conflict | 2026 | $125/b | $125/b |

Analysis: Why 2026 is Different

While the $214/b equivalent in 2008 remains the all-time “real” high, the current $125/b spike in 2026 is arguably more dangerous for three reasons:

- Velocity: Prices moved from $69 to $125 in weeks, rather than years, giving economies no time to adapt.

- Structural Fragility: Unlike the 1970s, modern “just-in-time” supply chains are highly sensitive to transport costs, amplifying the inflationary effect on groceries and consumer goods.

- The EV Tipping Point: In past crises (1979, 2008), consumers had no viable alternative to gasoline. In 2026, the high price is acting as a permanent “exit ramp,” driving users toward electric vehicles at a record pace.

The Takeaway: While we haven’t yet reached the inflation-adjusted peak of 2008, the 2026 crisis is unique because it may be the last time oil has the power to shock the global economy before the energy transition takes full hold.

Leave a Reply