High-Yield Everything: Breaking the 0.01% Habit

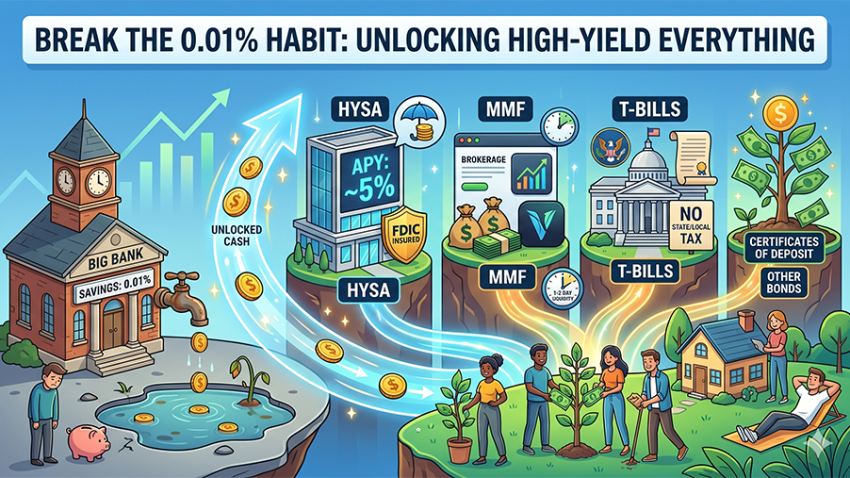

For years, the “Big Banks” have relied on inertia. They bet on the fact that moving your money is just enough of a hassle that you’ll leave your hard-earned cash sitting in a standard savings account, quietly earning a negligible 0.01% APY.

In an era where inflation has reset the baseline for purchasing power, leaving cash in a traditional savings account isn’t just “conservative”—it’s a guaranteed loss in real value. Fortunately, the financial landscape has shifted. Whether you are looking for liquidity, maximum safety, or the absolute highest yield, there are three primary vehicles for your “lazy” cash.

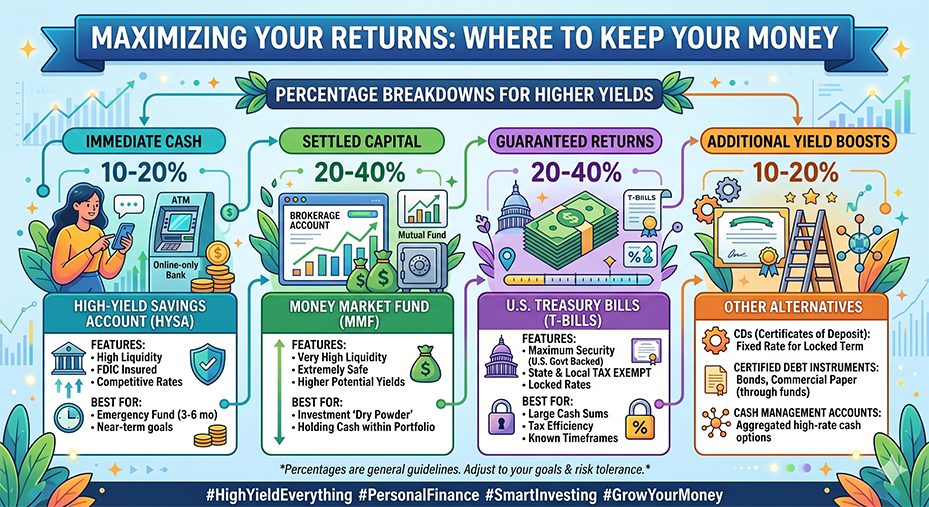

1. High-Yield Savings Accounts (HYSA)

The HYSA is the path of least resistance. Offered primarily by online-only banks (like Ally, Marcus, or SoFi) and some credit unions, these accounts function exactly like the savings account you already have, but with interest rates often 400x to 500x higher than traditional brick-and-mortar banks.

- Best for: Emergency funds and short-term savings (vacations, weddings).

- The Pro: FDIC insurance up to $250,000 provides the highest level of security.

- The Con: Rates are variable; they can drop quickly if the Federal Reserve cuts interest rates.

2. Money Market Funds (MMFs)

Not to be confused with a Money Market Account at a bank, a Money Market Fund is a type of mutual fund that invests in high-quality, short-term debt instruments (like U.S. Treasuries and commercial paper). You buy these through a brokerage account (Vanguard, Fidelity, Schwab).

- Best for: Investors who already have a brokerage account and want their “settled cash” to work harder.

- The Pro: Often yields slightly higher than HYSAs and offers extremely high liquidity.

- The Con: While they are managed to maintain a $1.00 net asset value (NAV), they are not technically FDIC-insured (though “breaking the buck” is historically rare).

3. Treasury Bills (T-Bills)

T-Bills are short-term debt obligations issued by the U.S. government with maturities ranging from four weeks to one year. You buy them at a discount and receive the full face value at maturity.

- Best for: Large sums of cash and those seeking tax efficiency.

- The Pro: Interest earned is exempt from state and local taxes. For investors in high-tax states like New York or California, the “tax-equivalent yield” often beats HYSAs and MMFs significantly.

- The Con: Your money is locked away until the bill matures (though you can sell them on the secondary market if needed).

Which One Should You Choose?

| Feature | HYSA | Money Market Fund | T-Bills |

| Safety | FDIC Insured | Very High (SIPC) | Backed by U.S. Govt |

| Liquidity | Immediate (1-3 days) | 1-2 days | At maturity (or secondary sale) |

| Tax Treatment | Fully Taxable | Fully Taxable | State/Local Exempt |

| Best Used For | 3-6 month emergency fund | Trading “dry powder” | Large tax-sensitive savings |

The “Moving” Strategy

You don’t have to move everything at once. A common professional strategy is the Three-Tiered Cash Approach:

- The Checking Account: Keep 1 month of expenses here (Yield: ~0%).

- The HYSA: Keep 2 months of expenses for immediate emergencies (Yield: ~4-5%).

- The T-Bill/MMF Ladder: Keep the rest of your long-term cash here to capture the highest yield and tax benefits.

Stop letting your bank profit off your inertia. In the current market, “High-Yield Everything” isn’t a luxury—it’s a fundamental requirement for a healthy portfolio.

Leave a Reply